11 Investment Tips for Couples With Differing Risk Tolerances

When it comes to marital finances, one important area to discuss is investments. Learn more about making a married investment strategy with your spouse!

When you’re married, it’s essential to make financial decisions together – but what if you have different risk tolerances?

Imagine this scenario: You and your spouse want to invest money together, but you have different opinions on investment risks. One of you wants to put all your money in a safe investment that guarantees no loss, while the other is willing to take more chances to see a higher return potential. What do you do?

Here are a few tips to get you and your partner started on the journey to building wealth together.

1. Define Your Financial Goals

What are your financial goals? Do you want to retire early? Build up an emergency fund? Save for your children’s education?

It’s essential to have a clear idea of what you want to achieve before you start investing. Once you know your goals, you can develop a plan to reach them.

For example, if you want to retire early, you’ll need to save more money and invest it more aggressively than if you’re saving for your children’s education.

Define SMART goals so you have the timeframe and purpose clarified, which can help you decide the best assets to achieve them.

If you’re not sure what your goals are, that’s OK. Start by thinking about what’s important to you and your family.

2. Embrace the Challenge Together

Work through your financial conflicts instead of avoiding or fighting about them. Investing as a married couple can be tricky.

A common approach many couples with differing risk tolerances might pursue is investing their money in separate accounts based on their preferences. While each partner managing their own investments might seem more straightforward, it is not a good idea to deal with your investment accounts separately.

All accounts are considered marital assets whether you title your accounts individually or together. Even 401(k)s, which almost all married couples handle independently, are considered marital assets.

Hence, the better approach is to have the challenging conversation upfront and come to an agreement.

A good relationship is built on working collaboratively toward financial objectives.

3. Decide the Rate of Return Needed

How much risk are you willing to take? This is a personal decision that only you can make.

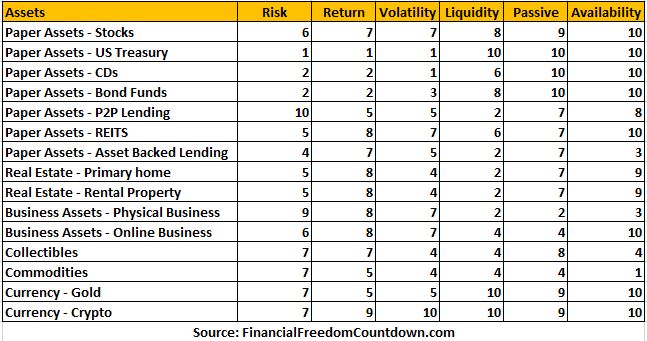

There are many different types of investments, each with its own risk level. Generally speaking, the higher the potential return, the higher the risk.

Knowing how much rate of return is needed to achieve your goal can help narrow down your investment choices and bring both partners on the same page.

You may be comfortable with a higher level of risk if you have a longer time horizon or if you’re investing for less time-sensitive goals. For example, if you’re saving for retirement, you may be willing to take more risks because you have a longer time horizon and can afford to weather the ups and downs of the market.

On the other hand, if you’re saving for a down payment on a house or your child’s tuition, you may want to take less risk because you have a shorter time horizon and can’t afford to lose any of your savings.

4. Compromise With Your Partner

Although different asset classes have specific risk-return profiles, you can further subdivide the asset class to satisfy both partners’ risk tolerance.

For example, the risk-taker partner might want to start investing in stocks; but the risk-averse partner is apprehensive. Compromise by investing in only blue-chip stocks or even restricting yourself to dividend stocks instead of the more volatile sector-specific stocks.

Similarly, although one spouse might be enthusiastic about buying rental properties and building a real estate empire, it might be more prudent to start small with real estate crowdfunding and invest in only debt deals where the collateral in the property secures your invested money.

Or, instead of diving headfirst into long-distance real estate investing, maybe try turnkey properties to dip your toes.

The important thing is that you’re both comfortable with the level of risk you’re taking.

5. Invest in What You Understand

It’s essential to invest in assets that you understand. If you don’t know how an investment works, you’re more likely to be hesitant to listen to your partner about their investment ideas.

For example, if you don’t understand how the stock market works, you’re more likely to panic and get upset with your partner, who advocated stock investments. You might insist on selling your stocks when they’re down instead of holding on and waiting for them to rebound.

The same goes for real estate investing. You’ll likely make poor investment decisions if you don’t understand how the market works.

Before investing in anything, ensure you understand how it works. There are a lot of resources available online and at your local library.

If you need help, talk to your financial advisor about investments that fit your level of understanding. Suppose your financial advisor cannot explain investment in plain language. In that case, it might be time to find an hourly paid fee-only advisor who takes the time to provide education while helping you find investments that meet your goals and risk tolerance.

6. Diversify Your Investments

Diversification is a crucial element of investing. It means spreading your money across different asset classes and investment vehicles.

For example, instead of investing all your money in stocks, you could diversify by investing in bonds, real estate, and cash.

Diversification helps to reduce risk because it ensures that you’re not putting all your eggs in one basket.

You have other investments to offset the loss if one investment loses money.

Diversification is crucial for investors with a high-risk tolerance because it helps to protect against losses in volatile markets. The key is to find an asset allocation that meets your goals and fits your risk tolerance.

7. Have a Plan B

No matter how well you diversify your investments, there’s always a chance that the market will go against you. That’s why it’s crucial to have a plan B.

Your plan B might be to sell some of your investments, take out a loan, or tap into your emergency fund.

Or it might be to hold on to your investments and ride out the market volatility.

The important thing is to have a written plan to know what to do if your investments start to lose money.

8. Write Down Your Investment Strategy

It is crucial to have your investment strategy in writing. This will help ensure that both partners are on the same page and are working towards the same goals.

Your investment strategy should include your investment goals, time horizon, and risk tolerance. It should also outline how you plan to achieve your goals and what types of investments you will use.

For example, if your goal is to retire early, your strategy might include saving a certain percentage of your monthly income and investing it in a mix of stocks and bonds.

If you’re saving for your child’s education, your strategy might involve investing in a 529 plan or opening a Roth IRA with conservative investments.

The additional benefit of having a written investment strategy in place is that when you encounter market volatility, both partners can read their written plan and be comfortable knowing it was a joint decision avoiding any blame game. Also, you can stay calm and avoid rash decisions to sell investments in a bear market.

9. Communicate Regularly With Your Spouse

It’s essential to communicate with your spouse about your financial goals, risk tolerance, and investment strategy.

If you’re not on the same page, making joint decisions about your finances will be difficult. You may end up arguing about money, which can strain your relationship.

There is no one-size-fits-all solution for investing as a married couple. The most important thing is to find a strategy that works for you and your spouse.

What works for one couple may not work for another. The key is to communicate openly and honestly. By doing so, you’ll be able to find an investment strategy that meets your needs and helps you reach your goals.

10. Separate Play Money Accounts

Although you may set joint financial goals and communicate often, there might still be disagreements on investment selections.

Having separate “play money” accounts is vital so each partner can make their own investment decisions without feeling constrained by the shared financial goals.

For example, one partner may want to invest in cryptocurrency while the other wants to save for financial independence. By setting aside a small amount of money in separate accounts, each partner can scratch their itch without jeopardizing the critical goals.

11. Your Relationship Is More Important Than Money

Consider investments not only in financial terms but also in your relationship. Is it really worth it if you make the best investment choices and accumulate a high net worth but end up divorcing your partner due to disagreements over investment choices?

Planning for future investments is critical, but it’s also vital that you appreciate and understand the value of your relationship. Don’t let money be an obstacle between you and your partner.

You may avoid a damaged relationship by learning to listen to your partner’s concerns and compromising to achieve your future objectives.

Summary

Investing as a married couple can be challenging, but it’s also an opportunity to build wealth together. By working through your differences and communicating openly, you can find a strategy that works for both of you.

Remember to communicate with your spouse, diversify your investments, and have a plan B if the market goes against you.

With a little effort, you can make investing as a married couple a positive experience.

Related tags: